Why does the 10-year US yield remain so high?

The 10-year US yield is a key determinant of FX moves

It tends to drop when the Fed prepares to cut its interest rates

Despite market expectations about the Fed, the 10-year US yield remains high

A stock market correction could be a catalyst for a sizeable drop in US yields

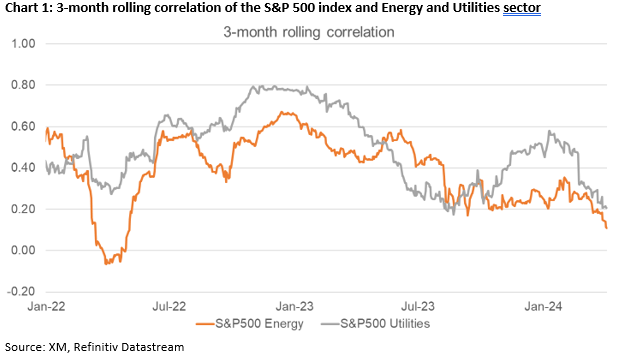

Should a correction in US equities take place, we could see safe haven flows materialize and pushing the 10-year US yield lower. In this case, defensive stocks could feature again in the headlines due to their historical performance in risk averse periods. As shown in Chart 1, the Energy and Utility sectors appear to enjoy the smallest correlation with the S&P 500 index.

Should a correction in US equities take place, we could see safe haven flows materialize and pushing the 10-year US yield lower. In this case, defensive stocks could feature again in the headlines due to their historical performance in risk averse periods. As shown in Chart 1, the Energy and Utility sectors appear to enjoy the smallest correlation with the S&P 500 index.

Related Assets

Latest News

Disclaimer: The XM Group entities provide execution-only service and access to our Online Trading Facility, permitting a person to view and/or use the content available on or via the website, is not intended to change or expand on this, nor does it change or expand on this. Such access and use are always subject to: (i) Terms and Conditions; (ii) Risk Warnings; and (iii) Full Disclaimer. Such content is therefore provided as no more than general information. Particularly, please be aware that the contents of our Online Trading Facility are neither a solicitation, nor an offer to enter any transactions on the financial markets. Trading on any financial market involves a significant level of risk to your capital.

All material published on our Online Trading Facility is intended for educational/informational purposes only, and does not contain – nor should it be considered as containing – financial, investment tax or trading advice and recommendations; or a record of our trading prices; or an offer of, or solicitation for, a transaction in any financial instruments; or unsolicited financial promotions to you.

Any third-party content, as well as content prepared by XM, such as: opinions, news, research, analyses, prices and other information or links to third-party sites contained on this website are provided on an “as-is” basis, as general market commentary, and do not constitute investment advice. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, it would be considered as marketing communication under the relevant laws and regulations. Please ensure that you have read and understood our Notification on Non-Independent Investment. Research and Risk Warning concerning the foregoing information, which can be accessed here.