Are there more AI growth opportunities to be priced into the markets?

Nvidia skyrockets and drives the S&P 500 to new records

Demand for chips continues to surge, AI enters consumers’ life

There maybe more AI growth opportunities to be priced in

But downside risks on high valuations and geopolitics do exist

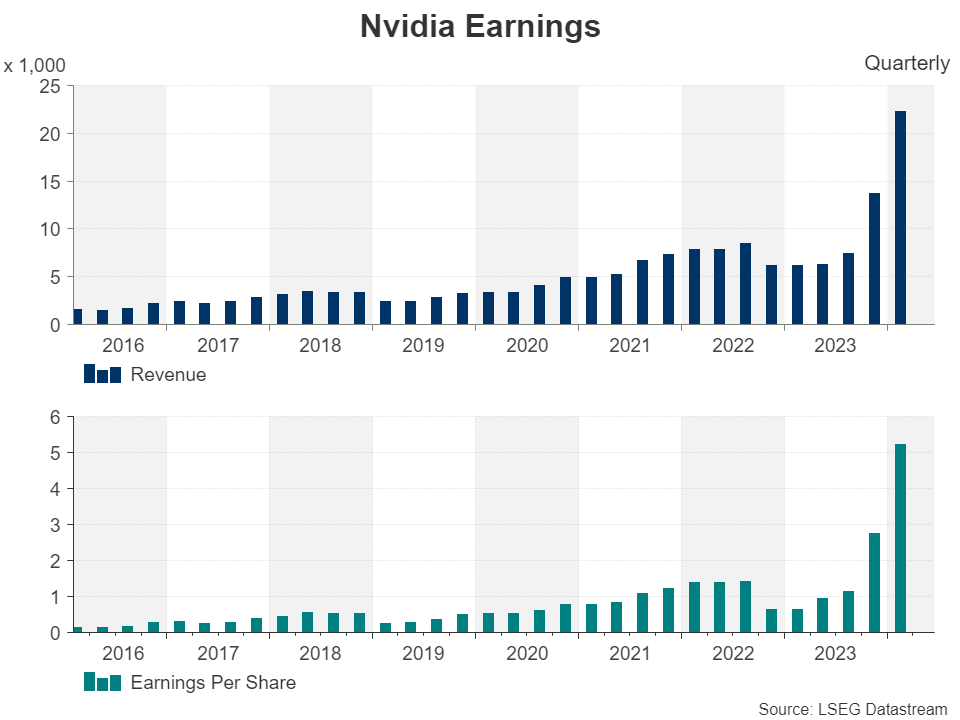

Just last week, the investor favorite Nvidia beat out Amazon and Alphabet to take the third place as the most valuable company in the US by market capitalization, and although the chipmaker’s stock pulled back before its earnings announcement, it rebounded to new record highs after the firm reported results better than Wall Street’s already ultra-optimistic forecasts.

This has propelled Wall Street higher, with the S&P 500 also entering uncharted territory and a question dominating almost all investors’ minds: How much longer can the artificial intelligence (AI) euphoria last? In other words, is the AI rally at its final stages or is there more fuel in the tank?

There is no simple and easy answer of course. On the one hand, there are those who believe that the turning point is near as the AI hype has already surpassed the 90s dot-com bubble as the top companies in the S&P 500 today are more overvalued than the top firms then. On the other hand, there are those saying that the earnings performance is suggesting that Wall Street is not in trouble, at least not yet.

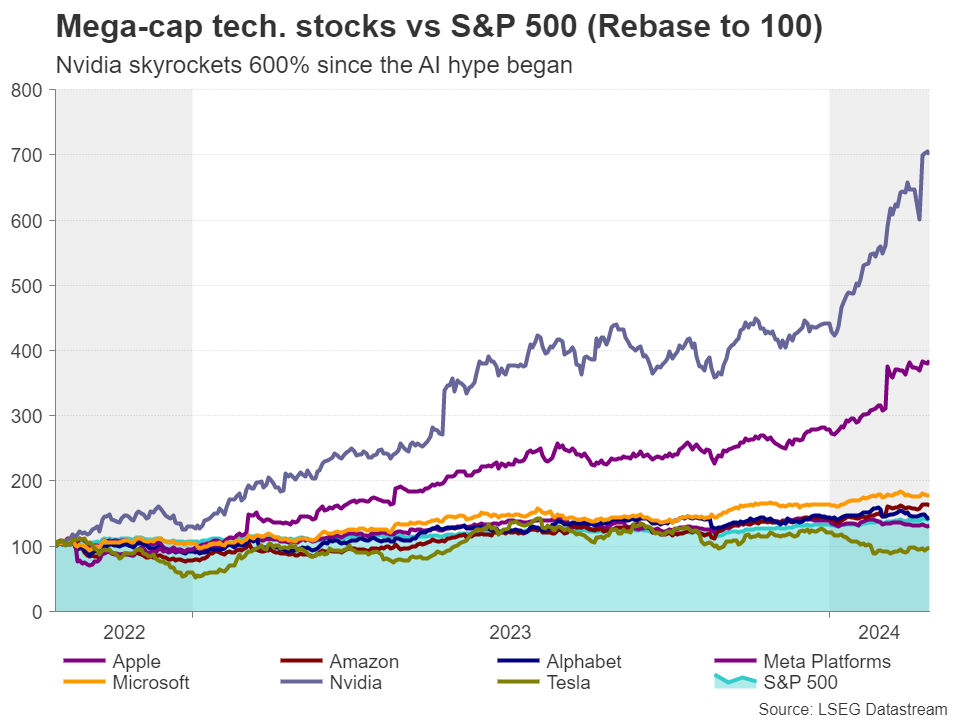

Demand for chips is surging worldwideThe euphoria around AI began in late 2022 after the release of ChatGPT 3.0, which opened the Pandora box regarding the possibilities of generative AI. Computer chips are the cornerstone component of generative AI systems, which require a lot of data processing and thus, with Nvidia being the dominant player – owning around 80% of market share – in AI chips, it’s shares have skyrocketed around 600% since the October 2022 lows, driving the S&P 500 up around 45%.

Demand for chips is surging across the globe, Nvidia’s CEO noted after the firm announced results for the last quarter of 2023, adding that they expect it to continue to be stronger than their supply. It is worth mentioning that earlier this month, Meta Platforms announced that they are planning to purchase more than $9bn worth of Nvidia graphic cards.

AI consumer-based products and roboticsWhat’s more, beyond the business-to-business part of chip making, the product has well reached consumers. Apart from the subscriptions to web-based and app-based chatbots, tech-giants have already begun introducing AI Phones, AI TVs, and AI PCs, all equipped with chips that are responsible for executing each product’s AI functionalities.

Robotics is also entering the discussion. Yes, creating larger robots is more expensive to develop than just chips for running software on computers, but the race is already on. Introducing robotics in large organizations is very likely to result in cost-savings, while also boosting productivity and thereby profitability.

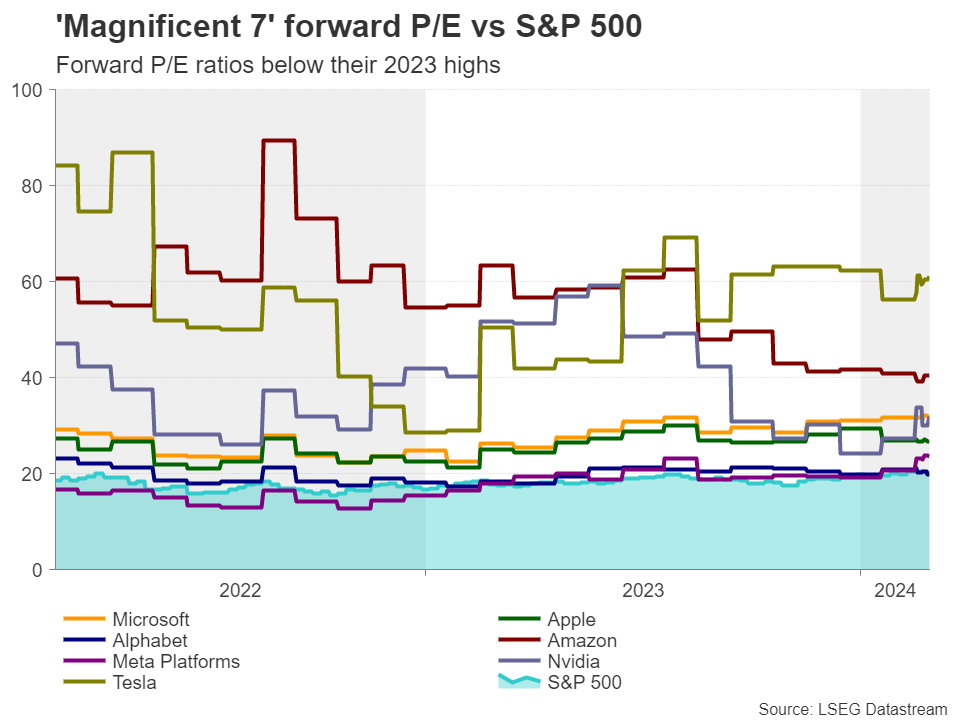

Could high valuations go even higher?Since the world might only just be starting to get a taste of how AI can impact our lives, are all the future growth opportunities of tech-firms already priced in or is there more? From a multiples’ perspective, although the forward price-to-earnings (P/E) ratios of almost all the ‘Magnificent 7’ tech giants are higher than the forward P/E ratio of the S&P 500, they are below their 2023 highs.

Nvidia is trading around 40 times the estimated earnings for next year, nearly double the 20.3x ratio of the S&P 500, but well below its own peak of 62.45x hit in 2023. This combined with the firm’s projections of growing cash flows for the quarters and years ahead suggests that Nvidia’s stock could continue to conquer new highs for a while longer, despite being by far the main gainer in the S&P 500.

The downside risksNonetheless, this doesn’t mean that there are no downside risks to this view. The vertical rally in Nvidia suggests that even a temporary let-up in investor demand for the stock could result in a sharp decline. For example, any tensions between China and Taiwan could trigger worries. China is not recognizing Taiwan as a sovereign state, while for the construction of their chips, most chipmakers rely on one company in Taiwan called TSMC (Taiwan Semiconductor Manufacturing Company).

Having said that though, even if chipmakers come under selling interest at some point soon, any declines could still be considered as a corrective phase rather than the beginning of a full-scale bear market. AI investors may abandon chipmakers like Nvidia, but they may decide to increase their exposure to more established tech stocks, like Alphabet, Amazon, Apple, Meta, and Microsoft, which are also expanding their business in the AI field.

Will a cheap Alphabet attract diverting flows?The best candidate for diverting flows may be Alphabet. Google’s parent seems to be the only ‘Magnificent 7’ stock that is cheaper than the S&P 500, while in terms of performance, it has not deviated much from the index, which means that it’s not stretched more than the broader market is.

Although Alphabet’s stock declined this week after the criticism of its “Gemini” AI system, it seems to be among the companies holding a massive opportunity in AI. What’s more, its free cash flows are expected to decline somewhat in the coming quarters of 2024, but to rebound in 2025, which could keep it attractive in the eyes of long-term investors.

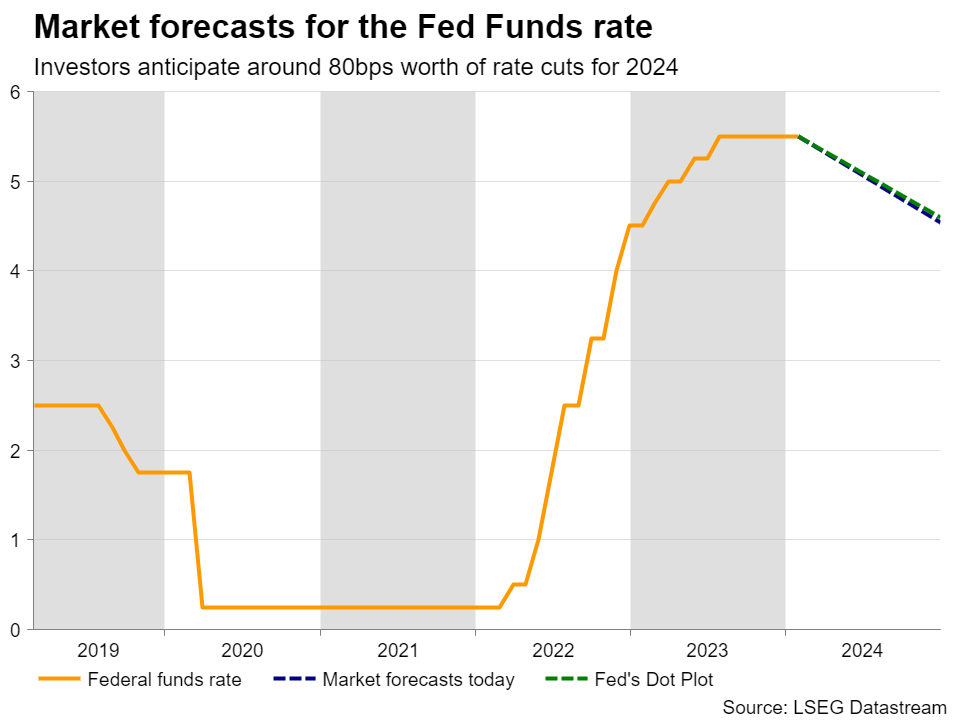

Fed rate cut expectations still a supportive variableAnother factor keeping high-growth tech firms attractive to investors may be expectations that the Fed will start lower interest rates at some point later this year.

The market has indeed priced out a significant amount of basis points worth of reductions since the start of the year but given that equity traders are mostly long-term investors, they may not be so concerned if rate cuts are delayed by a few months, especially if this is mainly due to a better-than-expected economic performance. The fact that no additional hikes are not on the table may be more than enough for them.

They may only decide to flee out of the stock market if expectations of delayed rate cuts are accompanied by disappointing growth estimates by big tech firms at the upcoming earnings seasons.Gerelateerde activa

Laatste nieuws

Disclaimer: De entiteiten van de XM Group bieden diensten en toegang tot ons online handelsplatform op basis van uitsluitend-uitvoering, waardoor een persoon de beschikbare content op of via de website kan bekijken en/of gebruiken, zonder dat dit is bedoeld voor wijziging of uitbreiding. Dergelijk(e) toegang en gebruik vallen onder: (i) de algemene voorwaarden; (ii) risicowaarschuwingen; en de (iii) volledige disclaimer. Dergelijke content wordt daarom alleen aangeboden als algemene informatie. Wees u er daarnaast vooral van bewust dat de inhoud op ons online handelsplatform geen verzoek of aanbieding omvat om transacties op de financiële markten uit te voeren. Het beleggen op welke financiële markt dan ook vormt een aanzienlijk risico voor uw vermogen.

Alle materialen die op ons online handelsplatform worden gepubliceerd zijn bedoeld voor educatieve/informatieve doeleinden en omvatten geen – en moeten niet worden beschouwd als het bevatten van – financieel, vermogensbelastings- of handelsadvies en aanbevelingen, of een overzicht van onze handelsprijzen, of een aanbod of aanvraag van een transactie in financiële instrumenten of ongevraagde financiële promoties voor u.

Alle content van derden, alsmede content die is voorbereid door XM, zoals opinies, nieuws, onderzoeken, analyses, prijzen en andere informatie of koppelingen naar externe websites op deze website worden aangeboden op een 'zoals-ze-zijn'-basis, als algemene marktcommentaren, en vormen geen beleggingsadvies. Voor zover dat content wordt beschouwd als beleggingsonderzoek, moet u zich ervan bewust zijn en accepteren dat de content niet bedoeld was en niet is voorbereid in overeenstemming met de wettelijke vereisten die zijn opgesteld om de onafhankelijkheid van beleggingsonderzoek te bevorderen en als zodanig onder de geldende wetgeving en richtlijnen moet worden beschouwd als marketingcommunicatie. Zorg ervoor dat u onze Mededeling over niet-onafhankelijk beleggingsonderzoek en risicowaarschuwing in verband met de voorgaande informatie doorneemt en begrijpt; die kunt u hier lezen.