Market continues to price in a plethora of rate cuts for 2024

Market is still in monetary easing mode despite fewer rate cuts priced in across the board

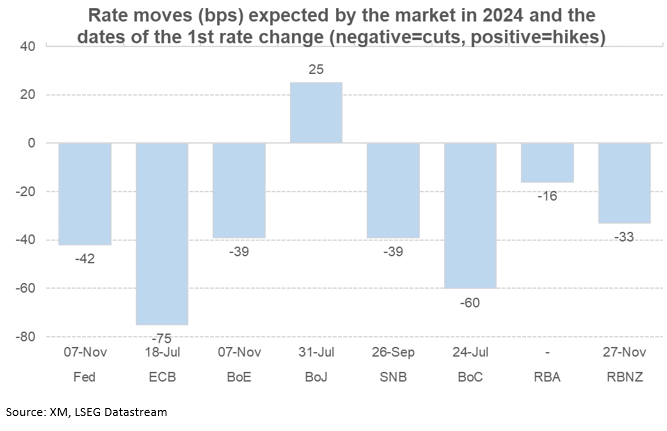

Divergent cut expectations for the Fed and the ECB, reflecting economic conditions

The ECB and the BoC are seen cutting in July; the RBA might not cut rates this year

BoJ is seen hiking again during 2024

BoC: two rate cuts and room for moreThe Bank of Canada is probably the most dovish central bank at this juncture. The significant progress made in inflation was acknowledged in the most recent BoC gathering with Governor Macklem talking about the need for further evidence of a sustainable easing inflation. When examining the domestic issues, especially the housing sector, one could say that the two rate cuts currently priced in are probably an underrepresentation of current situation and hence more rate cuts could be announced in 2024.BoE, SNB, RBNZ: one rate cut and done for 2024?These three diverse central banks are probably going to announce at least one rate cut in 2024. The UK continues to experience high inflation and a relatively low growth rate. Bank of England members are preparing for the much-touted rate cuts, but the threat of renewed inflationary pressures, on the back of the latest geopolitical developments supporting the recent oil price rally, is keeping them up at night.The year started with the market expecting almost four rate cuts by the Reserve Bank of New Zealand in 2024. Similarly to other central banks, inflation is proving stickier even though recent data is pointing to a weakness in consumer spending. Somewhat surprisingly, the RBNZ maintained its hawkishness at the recent meeting and poured cold water of dovish expectations. The market expects only 33bps of easing in 2024.The Swiss National Bank surprised the market with its March rate cut. The low inflation forecasts for both 2025 and 2026 could mean that the SNB is not done yet. Hence, the market is currently fully pricing in another 25bps rate cut by September with around 56% chance of one additional move by year-end.RBA: could it keep rates unchanged for 2024?The Reserve Bank of Australia was the last one to hike in 2023 and the market is only assigning a 64% probability for a 25bps rate cut in 2024. Such a move though could become even more improbable if China finally manages to return to growth, influencing its main trading partners and the commodity markets.BoJ: the market wants moreThe first rate hike since 2007 has opened the market’s appetite for further rate moves, which matches Governor’s Ueda current thinking. The market is pricing in at least another two 10bps rate hikes in 2024 with the current yen weakness, and its impact on imported inflation, potentially offering the Bank of Japan an excuse to do even more down the line.

BoC: two rate cuts and room for moreThe Bank of Canada is probably the most dovish central bank at this juncture. The significant progress made in inflation was acknowledged in the most recent BoC gathering with Governor Macklem talking about the need for further evidence of a sustainable easing inflation. When examining the domestic issues, especially the housing sector, one could say that the two rate cuts currently priced in are probably an underrepresentation of current situation and hence more rate cuts could be announced in 2024.BoE, SNB, RBNZ: one rate cut and done for 2024?These three diverse central banks are probably going to announce at least one rate cut in 2024. The UK continues to experience high inflation and a relatively low growth rate. Bank of England members are preparing for the much-touted rate cuts, but the threat of renewed inflationary pressures, on the back of the latest geopolitical developments supporting the recent oil price rally, is keeping them up at night.The year started with the market expecting almost four rate cuts by the Reserve Bank of New Zealand in 2024. Similarly to other central banks, inflation is proving stickier even though recent data is pointing to a weakness in consumer spending. Somewhat surprisingly, the RBNZ maintained its hawkishness at the recent meeting and poured cold water of dovish expectations. The market expects only 33bps of easing in 2024.The Swiss National Bank surprised the market with its March rate cut. The low inflation forecasts for both 2025 and 2026 could mean that the SNB is not done yet. Hence, the market is currently fully pricing in another 25bps rate cut by September with around 56% chance of one additional move by year-end.RBA: could it keep rates unchanged for 2024?The Reserve Bank of Australia was the last one to hike in 2023 and the market is only assigning a 64% probability for a 25bps rate cut in 2024. Such a move though could become even more improbable if China finally manages to return to growth, influencing its main trading partners and the commodity markets.BoJ: the market wants moreThe first rate hike since 2007 has opened the market’s appetite for further rate moves, which matches Governor’s Ueda current thinking. The market is pricing in at least another two 10bps rate hikes in 2024 with the current yen weakness, and its impact on imported inflation, potentially offering the Bank of Japan an excuse to do even more down the line.

Related Assets

Latest News

Disclaimer: The XM Group entities provide execution-only service and access to our Online Trading Facility, permitting a person to view and/or use the content available on or via the website, is not intended to change or expand on this, nor does it change or expand on this. Such access and use are always subject to: (i) Terms and Conditions; (ii) Risk Warnings; and (iii) Full Disclaimer. Such content is therefore provided as no more than general information. Particularly, please be aware that the contents of our Online Trading Facility are neither a solicitation, nor an offer to enter any transactions on the financial markets. Trading on any financial market involves a significant level of risk to your capital.

All material published on our Online Trading Facility is intended for educational/informational purposes only, and does not contain – nor should it be considered as containing – financial, investment tax or trading advice and recommendations; or a record of our trading prices; or an offer of, or solicitation for, a transaction in any financial instruments; or unsolicited financial promotions to you.

Any third-party content, as well as content prepared by XM, such as: opinions, news, research, analyses, prices and other information or links to third-party sites contained on this website are provided on an “as-is” basis, as general market commentary, and do not constitute investment advice. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, it would be considered as marketing communication under the relevant laws and regulations. Please ensure that you have read and understood our Notification on Non-Independent Investment. Research and Risk Warning concerning the foregoing information, which can be accessed here.