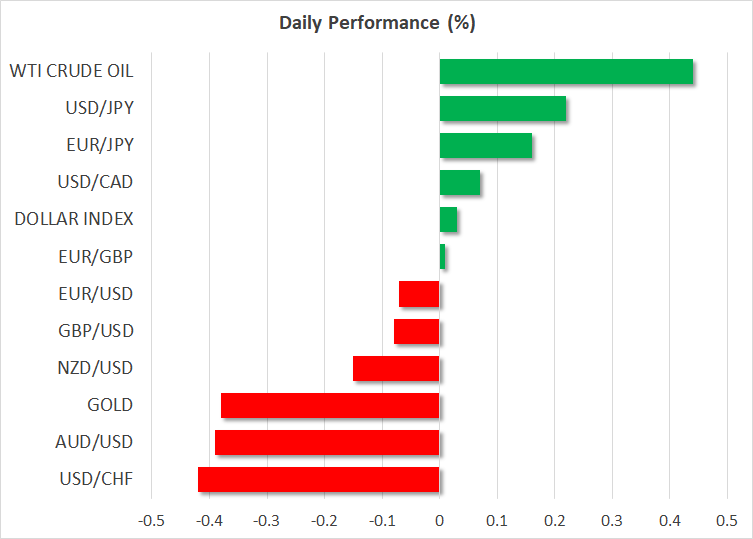

Market Comment – Gold sinks amid stronger dollar and rising yields

Gold prices fall further, pressured on multiple fronts

Yen loses ground after Bank of Japan intervenes in bond market

Dollar stable ahead of some key data and Fed chief Powell

Gold realigns with fundamentals

The final quarter of the year begins with familiar themes in global markets. A relentless rally in US bond yields driven by increased debt supply, renewed concerns about China’s economic health, and a sinking Japanese yen continue to dominate the agenda for traders.

Gold absorbed significant damage last week, falling sharply to hit its lowest levels since March as it started to realign with its gloomy fundamentals. For months now, gold kept defying the downside pressure exerted by soaring real yields and an appreciating US dollar, as sovereign purchases by central banks offset some of the selling pressure.

It appears that central bank purchases have finally dried up, leaving gold to fend for itself in an environment of sky-high real yields. The result was a catastrophe, with bullion losing 4% of its value in a single week. Looking at the charts, the next major region on the downside is near $1,810.

The precious metal extended its losses on Monday, following a last-minute political deal to avert a US government shutdown, which helped calm some nerves in the markets and lift Wall Street futures. That said, this bill will fund the government only for 45 days, so investors will see another replay of the shutdown movie in mid-November.

Yen hits fresh lows, China PMIs mixed

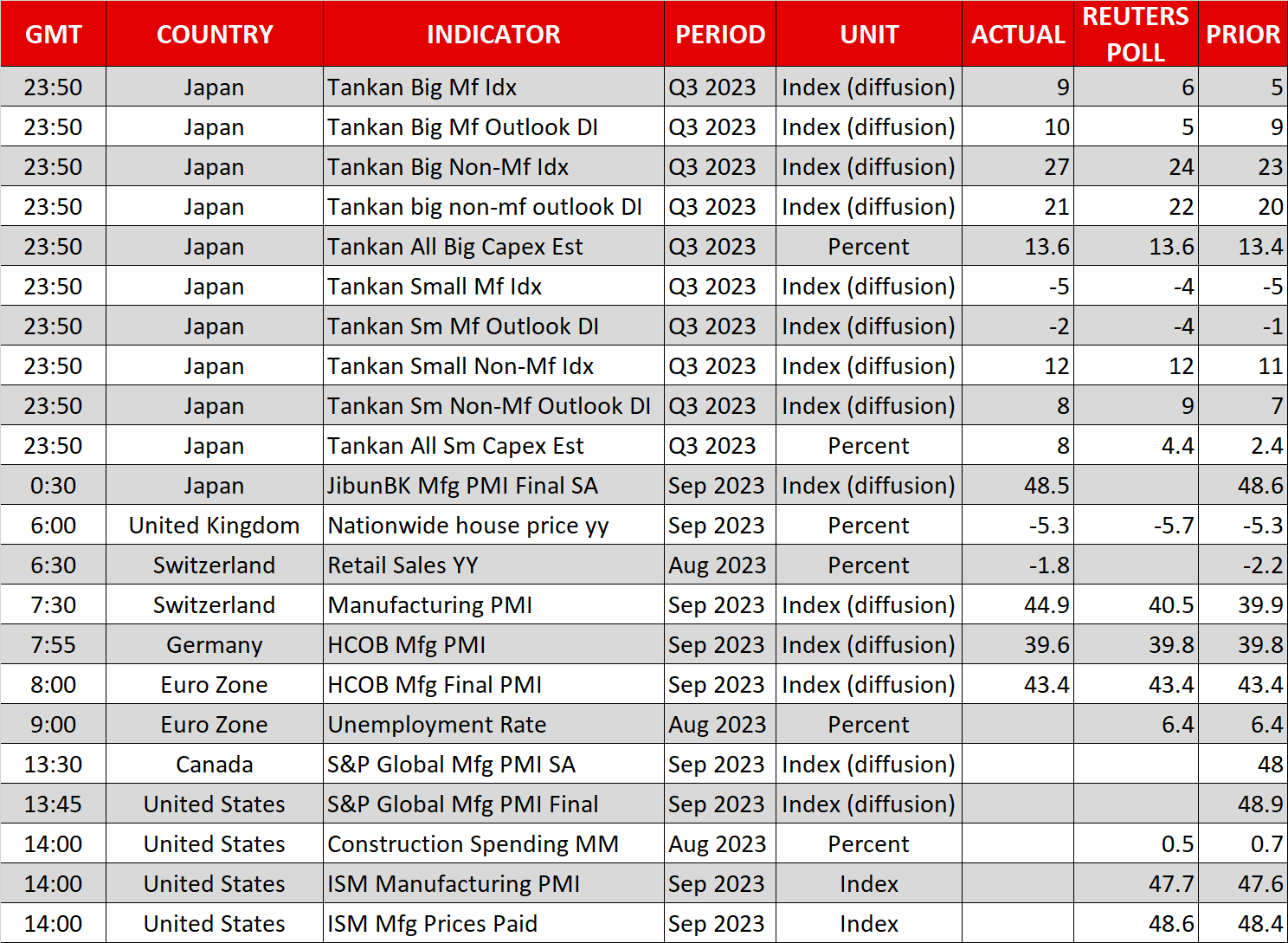

In the FX complex, the Japanese yen continues to bleed. The yen fell to its lowest levels in a year against the US dollar on Monday, after the Bank of Japan once again intervened in the bond market to prevent Japanese yields from rising too much. The move followed the quarterly Tankan survey, which revealed improving business morale.

With the BoJ preventing domestic yields from rallying while US yields keep charging higher, interest rate differentials continue to widen against the yen and the rally in oil prices has made matters worse for the energy-importing currency.

Even though dollar/yen is now trading just below the 150 level that triggered FX intervention last year, the risk of intervention seems lower this time. The speed of the yen’s depreciation has been much slower this year and the verbal warnings from Tokyo have been more measured in tone. Hence, the intervention line has likely shifted higher.

In China, the latest business surveys painted a mixed picture. On the bright side, the PMIs fueled optimism that the manufacturing sector has started to bottom out. However, the services sector is losing steam and barely avoided contraction in September, which suggests that the broader outlook remains grim.

Dollar stable, RBA decision in focus

Despite a PCE inflation report that was slightly colder than expected on Friday, dimming the prospect that the Fed will raise rates again, the US dollar still managed to close the week with impressive gains.

Euro/dollar has declined for eleven weeks now, as differentials in economic growth and interest rates increasingly turned in the dollar’s favor. The American economy has been shielded by the government’s massive deficit spending and the slower transmission of high interest rates thanks to fixed-rate mortgages, but Europe is feeling the burn of adjustable rates and elevated energy prices.

Business surveys suggest these economic trends might persist for some time and with US debt issuance also set to remain at stratospheric levels this quarter, maintaining the upward pressure on US yields, the fundamentals still argue for a weaker euro/dollar.

As for today, the spotlight will fall on the ISM manufacturing survey, which will be followed by some remarks from Fed Chairman Powell at 15:00 GMT. That said, he will be meeting with workers and small business owners, so he might avoid monetary policy comments. Beyond that, traders will turn to the Reserve Bank of Australia, which will announce its decision on Tuesday.

Related Assets

Latest News

Disclaimer: The XM Group entities provide execution-only service and access to our Online Trading Facility, permitting a person to view and/or use the content available on or via the website, is not intended to change or expand on this, nor does it change or expand on this. Such access and use are always subject to: (i) Terms and Conditions; (ii) Risk Warnings; and (iii) Full Disclaimer. Such content is therefore provided as no more than general information. Particularly, please be aware that the contents of our Online Trading Facility are neither a solicitation, nor an offer to enter any transactions on the financial markets. Trading on any financial market involves a significant level of risk to your capital.

All material published on our Online Trading Facility is intended for educational/informational purposes only, and does not contain – nor should it be considered as containing – financial, investment tax or trading advice and recommendations; or a record of our trading prices; or an offer of, or solicitation for, a transaction in any financial instruments; or unsolicited financial promotions to you.

Any third-party content, as well as content prepared by XM, such as: opinions, news, research, analyses, prices and other information or links to third-party sites contained on this website are provided on an “as-is” basis, as general market commentary, and do not constitute investment advice. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, it would be considered as marketing communication under the relevant laws and regulations. Please ensure that you have read and understood our Notification on Non-Independent Investment. Research and Risk Warning concerning the foregoing information, which can be accessed here.