Could a strong inflation print reignite hawkish RBA expectations? – Forex News Preview

The RBA holds its monthly meeting on June 6 with the market expecting no change at the current 3.85% cash target rate. A total of 20 bps of rate hikes are priced in by the September 2023 meeting, implying an 80% chance of a full 25 bps rate hike. While we don’t exclude a surprise at next week’s meeting, the overall environment appears to be less supportive of hawkish surprises. Especially as the neighbouring RBNZ has probably announced its last hike in the current cycle and the Fed is almost ready to keep rates unchanged in its upcoming meeting for the first time since March 2022.

However, as seen in early May, the RBA could pull another rate hike out of the hat. The bar though appears to be higher now, especially as the preliminary PMIs were not a pleasant reading, unemployment is edging higher again and retail sales surprised on the downside. But the key data print remains inflation.

Monthly CPI is not really “monthly CPI”The monthly CPI figure will be released on Wednesday, and it is expected to remain comfortably above 6% and very close to April's 6.3% year-on-year change. Confirmation of the consensus forecast, or an even lower print, would probably cement the very low market expectations for the June meeting. On the other hand, a stronger print, especially if it climbs above 7%, would hesitantly bring back to the table the possibility of another rate hike, giving the aussie a much-needed boost.

The market is very keen on the monthly inflation updates, but here lies a critical issue for the RBA. The official inflation figures for Australia are published on a quarterly basis. In October 2022 the Bureau of Statistics started to publish a monthly figure which is only two-thirds representative of the quarterly CPI basket. This means that revisions take place and could be significant.

Housing sector still under pressureAnother sector that continues to get significant airtime, mostly for negative reasons, is the housing sector. With the building approvals moving again in negative territory, the focus now turns to home loans. This tends to be a leading indicator of demand in the housing sector with the March figure finally showing a positive change after 9 straight months of negative growth. The year-on-year figures remain almost 25% lower, but another positive monthly change would be seen as a positive signal despite the aggressive rate hikes.

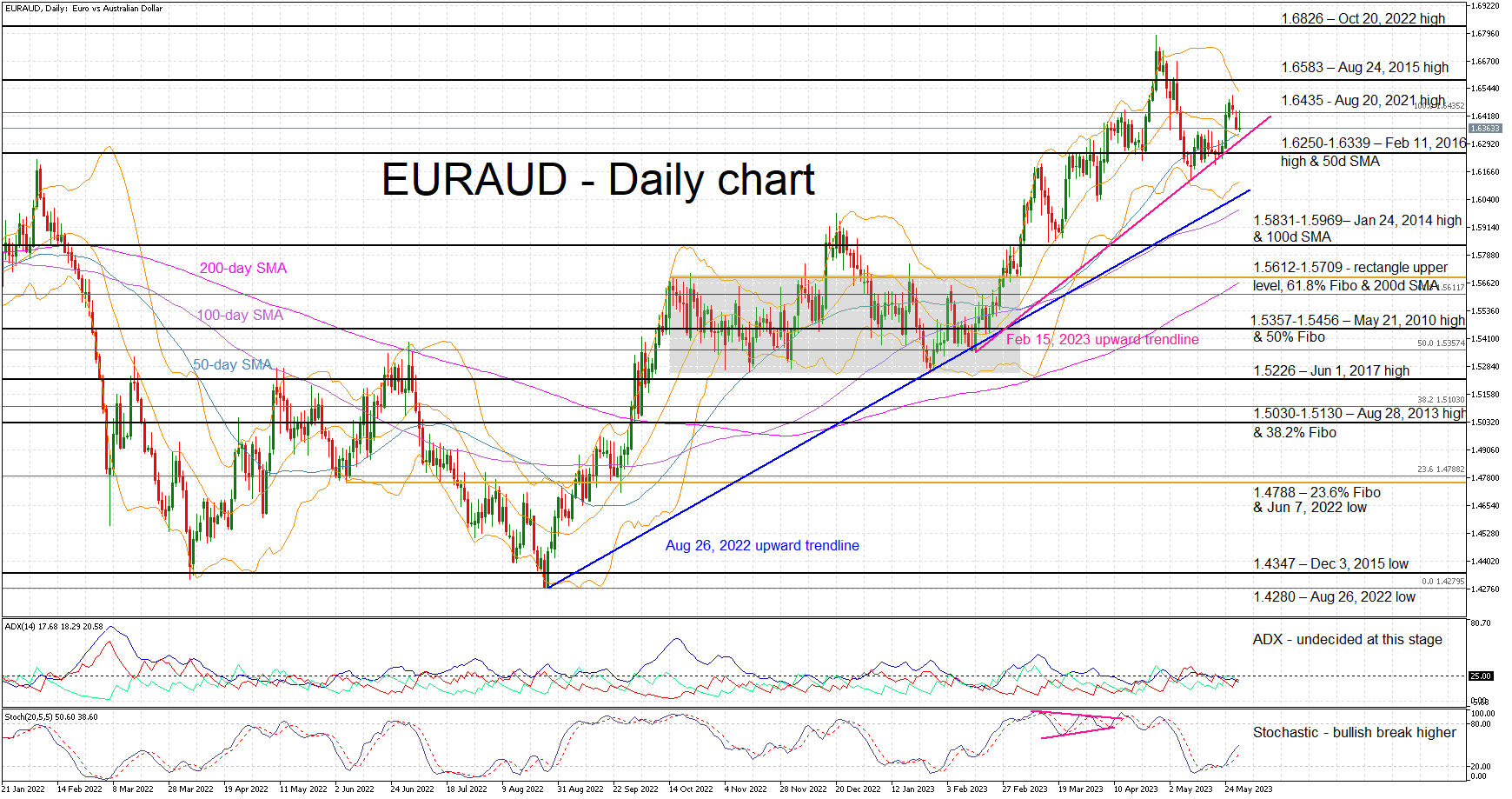

Euro/aussie experiencing bullish pressureThe aussie has been on the back foot since August 2022, underperforming the euro by around 15%. Recently, it has been trying to recover part of these losses, especially following the recent streak of weak euro area data. However, any attempt for a significant correction at the euro/aussie pair has halted at the February 15, 2023 upward sloping trendline. In addition, with the stochastic edging almost vertically higher, the onus is on aussie bulls to stop this pair from recording higher highs.

A positive set of data this week, and particularly an upside inflation surprise, would help the aussie bulls retest and potentially break the aforementioned trendline and the busy 1.6250-1.6339 area. On the other hand, weak data figures, which would essentially negate any change for a surprise rate hike at the next week’s meeting, would open the door for a break of the 1.6583 level and a retest of the October 20, 2022 high at 1.6826.

Related Assets

Latest News

Disclaimer: The XM Group entities provide execution-only service and access to our Online Trading Facility, permitting a person to view and/or use the content available on or via the website, is not intended to change or expand on this, nor does it change or expand on this. Such access and use are always subject to: (i) Terms and Conditions; (ii) Risk Warnings; and (iii) Full Disclaimer. Such content is therefore provided as no more than general information. Particularly, please be aware that the contents of our Online Trading Facility are neither a solicitation, nor an offer to enter any transactions on the financial markets. Trading on any financial market involves a significant level of risk to your capital.

All material published on our Online Trading Facility is intended for educational/informational purposes only, and does not contain – nor should it be considered as containing – financial, investment tax or trading advice and recommendations; or a record of our trading prices; or an offer of, or solicitation for, a transaction in any financial instruments; or unsolicited financial promotions to you.

Any third-party content, as well as content prepared by XM, such as: opinions, news, research, analyses, prices and other information or links to third-party sites contained on this website are provided on an “as-is” basis, as general market commentary, and do not constitute investment advice. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, it would be considered as marketing communication under the relevant laws and regulations. Please ensure that you have read and understood our Notification on Non-Independent Investment. Research and Risk Warning concerning the foregoing information, which can be accessed here.