Week Ahead – US inflation report coming up as dollar storms higher

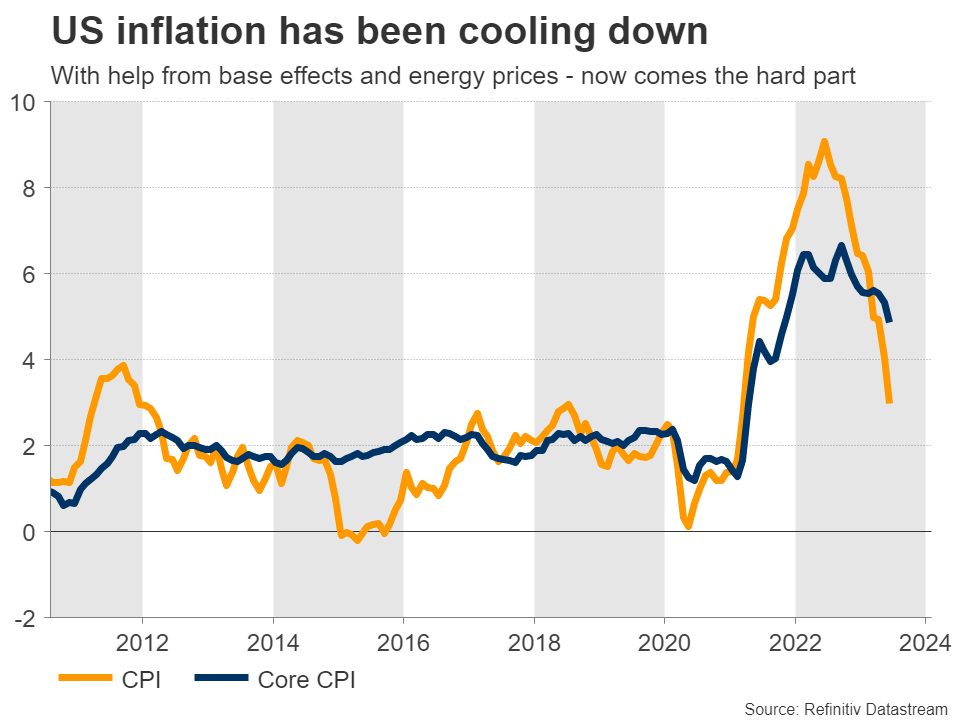

Fortunately, the outlook will become clearer on Thursday with the next round of US inflation data. Forecasts suggest that both the headline and core CPI rates rose by 0.2% in monthly terms in July, which would translate into an increase in the yearly CPI rate but a decline in the core rate. Specifically, the core rate is expected to drop to 4.7%, from 4.8% previously. Yet, the risks surrounding these forecasts might be tilted to the upside. The Cleveland Fed has a model that attempts to forecast inflation, and it currently points to an increase of 0.4% for both the headline and core CPI rates, in monthly terms. Historically, this model tends to be quite accurate, so there is some scope for a hotter-than-anticipated CPI report. In the FX arena, this could translate into a stronger US dollar as traders recalibrate the Fed’s interest rate path in a higher-for-longer direction, lifting US yields even higher.

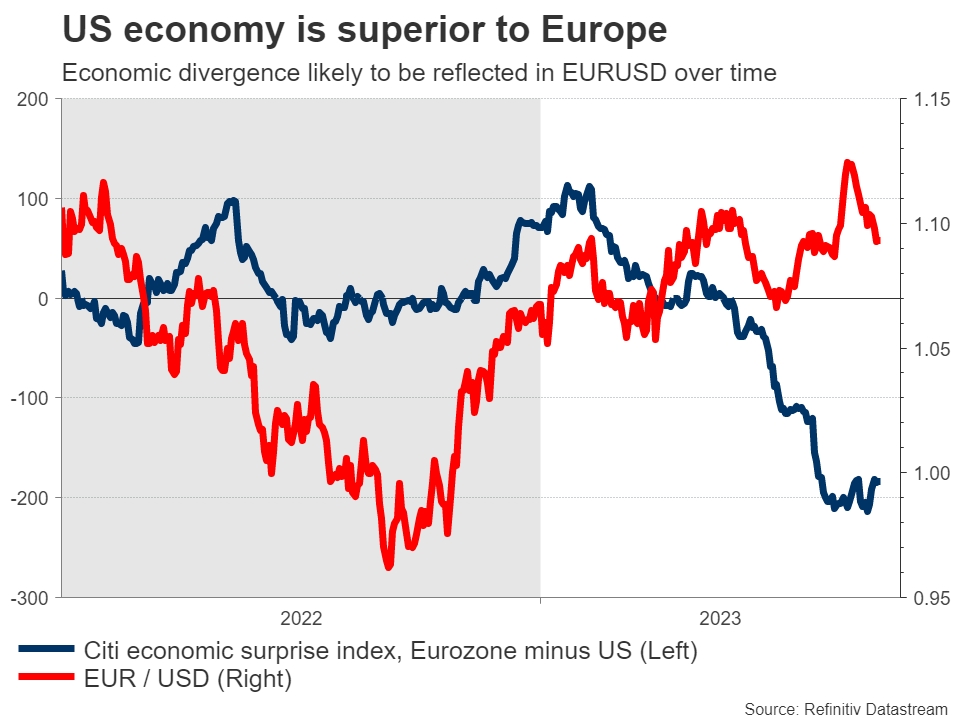

Fortunately, the outlook will become clearer on Thursday with the next round of US inflation data. Forecasts suggest that both the headline and core CPI rates rose by 0.2% in monthly terms in July, which would translate into an increase in the yearly CPI rate but a decline in the core rate. Specifically, the core rate is expected to drop to 4.7%, from 4.8% previously. Yet, the risks surrounding these forecasts might be tilted to the upside. The Cleveland Fed has a model that attempts to forecast inflation, and it currently points to an increase of 0.4% for both the headline and core CPI rates, in monthly terms. Historically, this model tends to be quite accurate, so there is some scope for a hotter-than-anticipated CPI report. In the FX arena, this could translate into a stronger US dollar as traders recalibrate the Fed’s interest rate path in a higher-for-longer direction, lifting US yields even higher.  Overall, it is becoming increasingly clear that the American economy remains resilient, with economic growth running around 2%, solid consumption trends, and a labor market that is in good shape. In contrast, business surveys suggest the European economy is slowly descending into a recession, as the downturn in manufacturing has started to infect the services sector. If this relative US outperformance continues to play out, it is likely to be reflected in the FX market eventually, putting downward pressure on euro/dollar. British GDP eyed after BoE disappointsIn the United Kingdom, GDP stats for Q2 will hit the markets on Friday. This will be an important piece of the puzzle for the Bank of England, after the central bank raised interest rates in a cautious manner this week, dealing a blow to the British pound. Still, the pound remains the second-best performing major currency this year, behind the Swiss franc. This powerful rally reflects two elements - expectations that the BoE will push rates higher than other central banks because the UK has a bigger inflation problem, and the cheerful tone in stock markets that tends to benefit the risk-sensitive pound.

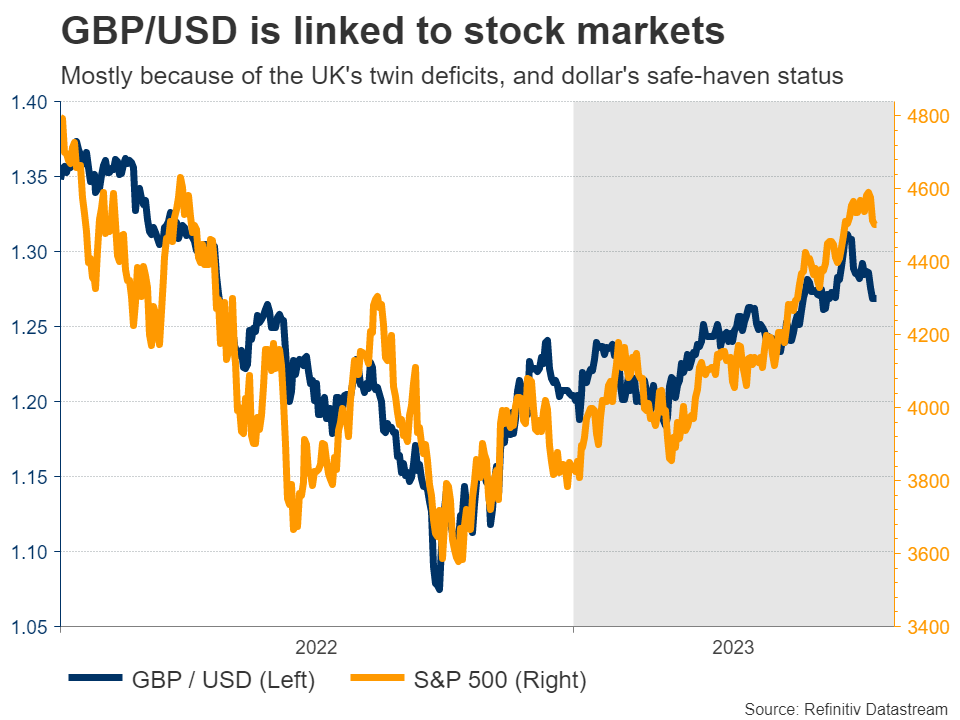

Overall, it is becoming increasingly clear that the American economy remains resilient, with economic growth running around 2%, solid consumption trends, and a labor market that is in good shape. In contrast, business surveys suggest the European economy is slowly descending into a recession, as the downturn in manufacturing has started to infect the services sector. If this relative US outperformance continues to play out, it is likely to be reflected in the FX market eventually, putting downward pressure on euro/dollar. British GDP eyed after BoE disappointsIn the United Kingdom, GDP stats for Q2 will hit the markets on Friday. This will be an important piece of the puzzle for the Bank of England, after the central bank raised interest rates in a cautious manner this week, dealing a blow to the British pound. Still, the pound remains the second-best performing major currency this year, behind the Swiss franc. This powerful rally reflects two elements - expectations that the BoE will push rates higher than other central banks because the UK has a bigger inflation problem, and the cheerful tone in stock markets that tends to benefit the risk-sensitive pound.  Now the question is whether these elements will remain in force moving forward. Business surveys suggest the British economy is set to “flatline at best in the coming months”, which is not exactly inspiring. Meanwhile, inflationary pressures continue to rage, painting the picture of an economy that is about to experience a period of stagflation. Similarly, stock markets seem vulnerable to a correction after a stunning rally this year. This rally was not backed by rising earnings, so valuations simply became more expensive. Therefore, if yields keep rising, that could spark a correction in stocks that in turn inflicts collateral damage on risk-linked currencies like sterling. Japanese and Chinese releasesCrossing into Asia, the ball will get rolling on Monday with the Bank of Japan’s summary of economic opinions for the July meeting, where the central bank raised its effective ceiling on Japanese yields.

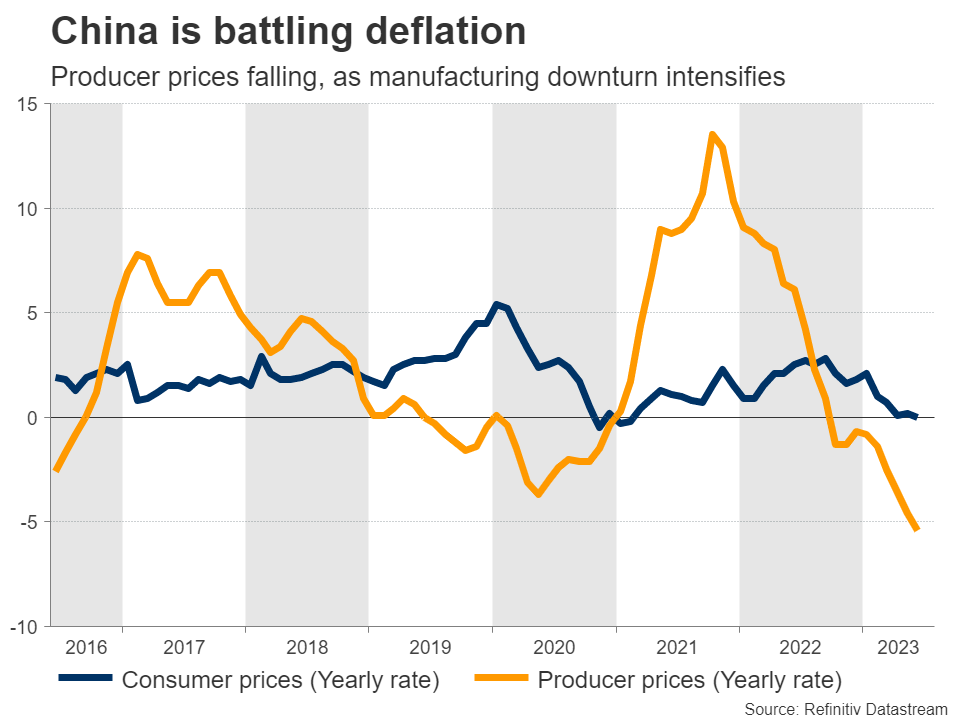

Now the question is whether these elements will remain in force moving forward. Business surveys suggest the British economy is set to “flatline at best in the coming months”, which is not exactly inspiring. Meanwhile, inflationary pressures continue to rage, painting the picture of an economy that is about to experience a period of stagflation. Similarly, stock markets seem vulnerable to a correction after a stunning rally this year. This rally was not backed by rising earnings, so valuations simply became more expensive. Therefore, if yields keep rising, that could spark a correction in stocks that in turn inflicts collateral damage on risk-linked currencies like sterling. Japanese and Chinese releasesCrossing into Asia, the ball will get rolling on Monday with the Bank of Japan’s summary of economic opinions for the July meeting, where the central bank raised its effective ceiling on Japanese yields.  Over in China, the downturn in the manufacturing sector has taken a heavy toll on the economy and the stimulus measures announced by Beijing so far seem insufficient to turn the tide. This puts extra emphasis on the trade and inflation numbers for July, which will be released on Tuesday and Wednesday, respectively. Another disappointing dataset could amplify concerns about the health of the world’s second-largest economy, and by extension, keep China-sensitive currencies like the Australian dollar under pressure.

Over in China, the downturn in the manufacturing sector has taken a heavy toll on the economy and the stimulus measures announced by Beijing so far seem insufficient to turn the tide. This puts extra emphasis on the trade and inflation numbers for July, which will be released on Tuesday and Wednesday, respectively. Another disappointing dataset could amplify concerns about the health of the world’s second-largest economy, and by extension, keep China-sensitive currencies like the Australian dollar under pressure. Related Assets

Latest News

Disclaimer: The XM Group entities provide execution-only service and access to our Online Trading Facility, permitting a person to view and/or use the content available on or via the website, is not intended to change or expand on this, nor does it change or expand on this. Such access and use are always subject to: (i) Terms and Conditions; (ii) Risk Warnings; and (iii) Full Disclaimer. Such content is therefore provided as no more than general information. Particularly, please be aware that the contents of our Online Trading Facility are neither a solicitation, nor an offer to enter any transactions on the financial markets. Trading on any financial market involves a significant level of risk to your capital.

All material published on our Online Trading Facility is intended for educational/informational purposes only, and does not contain – nor should it be considered as containing – financial, investment tax or trading advice and recommendations; or a record of our trading prices; or an offer of, or solicitation for, a transaction in any financial instruments; or unsolicited financial promotions to you.

Any third-party content, as well as content prepared by XM, such as: opinions, news, research, analyses, prices and other information or links to third-party sites contained on this website are provided on an “as-is” basis, as general market commentary, and do not constitute investment advice. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, it would be considered as marketing communication under the relevant laws and regulations. Please ensure that you have read and understood our Notification on Non-Independent Investment. Research and Risk Warning concerning the foregoing information, which can be accessed here.